Introduction: Why Many Car Owners Get Less Claim Amount Than Expected

You buy car insurance thinking that if something happens — like theft or a total loss accident — the insurance company will compensate you based on your car’s actual market value.

But when a major claim occurs, many vehicle owners in Pakistan are shocked to learn that the settlement amount is much lower than expected.

Why does this happen?

In most cases, it’s because of something called Insured Declared Value (IDV).

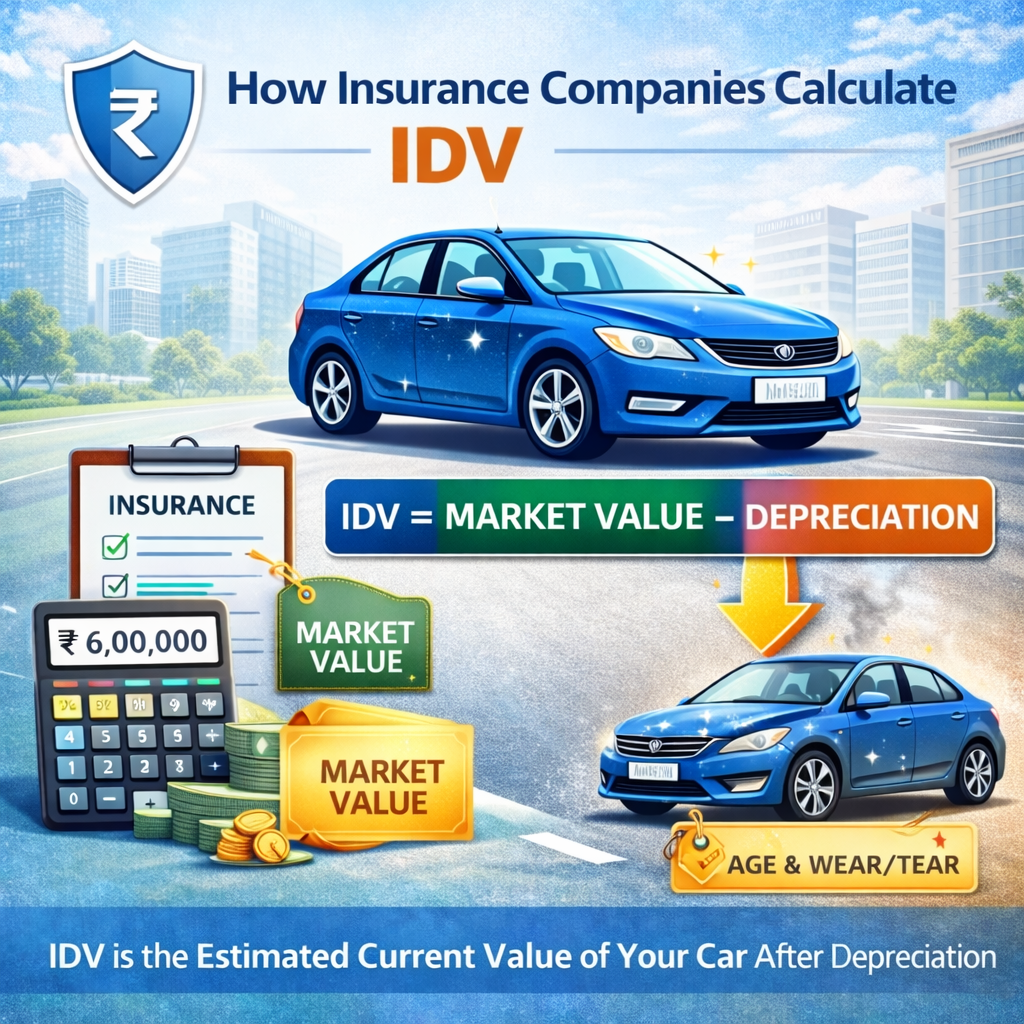

IDV is the maximum amount your insurance company will pay you if your car is stolen or declared a total loss after an accident.

Many policyholders do not fully understand how insurance companies calculate IDV — and this lack of awareness can lead to:

- Lower claim settlements

- Incorrect premium payments

- Financial loss after major accidents

- Over- or under-insured vehicles

Understanding how IDV is calculated is essential to ensure that your insurance policy provides adequate financial protection when you need it the most.

How Comprehensive Car Insurance Works

Comprehensive car insurance provides financial protection against:

- Accidental damage

- Theft

- Fire

- Natural disasters

- Vandalism

- Total loss

- Third-party damage

When issuing a comprehensive policy, insurers determine your vehicle’s IDV — which becomes the basis for:

- Premium calculation

- Claim settlement

- Coverage limits

If your vehicle is declared a total loss or stolen, the insurer compensates you up to the IDV amount mentioned in your policy document.

How Insurance Companies Calculate IDV

Insurance companies calculate IDV based on the following factors:

- Manufacturer’s Selling Price (Excluding Taxes)

The original showroom price of the vehicle is considered without including registration costs or road taxes. - Depreciation Based on Vehicle Age

Depreciation is applied according to how old the vehicle is. Typical depreciation structure: Vehicle AgeDepreciation AppliedUp to 6 Months5%6 Months – 1 Year15%1 – 2 Years20%2 – 3 Years30%3 – 4 Years40%4 – 5 Years50%Above 5 YearsMarket Value - Vehicle Condition

Insurers may assess the physical condition during inspection. - Make and Model

Imported vehicles may depreciate differently compared to locally assembled cars. - Location and Usage

Vehicles used in urban areas may have different risk profiles.

The final IDV represents the approximate current market value of the insured vehicle.

Who Should Buy It?

Understanding IDV is particularly important for:

- New car owners

- Owners of high-value vehicles

- Bank-financed vehicle holders

- Individuals planning policy renewal

- Owners of imported vehicles

- Daily commuters

Accurate IDV selection ensures that your policy reflects your vehicle’s actual replacement value.

Benefits

Correct IDV calculation provides several advantages:

- Accurate claim settlement

- Balanced premium cost

- Financial protection in total loss cases

- Reduced risk of underinsurance

- Transparent policy coverage

Choosing the correct IDV helps ensure that you are neither paying excess premium nor risking inadequate compensation.

Limitations

Despite its importance, IDV has certain limitations:

- It decreases annually due to depreciation

- Market value fluctuations may affect settlement

- Overstating IDV may increase premium unnecessarily

- Understating IDV may reduce claim amount

- Inspection may be required for older vehicles

Policyholders should review IDV during each renewal cycle.

Estimated Cost in Pakistan

Premium is directly influenced by the selected IDV.

| IDV Value | Estimated Annual Premium |

|---|---|

| PKR 1,000,000 | PKR 25,000 – 35,000 |

| PKR 1,500,000 | PKR 35,000 – 50,000 |

| PKR 2,000,000 | PKR 50,000 – 70,000 |

| PKR 3,000,000 | PKR 70,000 – 100,000 |

Higher IDV generally results in higher premium — but also higher claim protection.

Factors That Affect Premium

Insurance premiums are affected by:

- Insured Declared Value

- Vehicle age

- Engine capacity

- Claim history

- Driver profile

- Security features

- Geographic location

- Policy add-ons

Maintaining an accurate IDV can help manage premium costs effectively.

Real Example Scenario

Consider the case of Hamza, who owns a 2018 Honda Civic.

At renewal, he selected a lower IDV of PKR 1,200,000 to reduce premium cost.

Unfortunately, his car was stolen six months later.

Since the policy IDV was lower than the market value, the insurer compensated him only up to PKR 1,200,000 — resulting in a financial shortfall compared to the car’s actual resale price.

This highlights the importance of choosing an appropriate IDV.

Tips Before Buying

When selecting IDV:

- Check current market value

- Avoid under-declaring value

- Compare insurer quotes

- Confirm depreciation rates

- Request vehicle inspection if needed

- Review IDV at renewal

- Maintain service history

These steps can help ensure adequate financial coverage.

FAQs

Can I choose my own IDV?

Policyholders may suggest an IDV, but insurers usually approve it based on market assessment.

Does higher IDV increase premium?

Yes, higher IDV leads to a higher premium.

Is IDV applicable in partial damage claims?

No, IDV applies mainly in total loss or theft cases.

Should IDV be updated annually?

Yes, it should be reviewed during each policy renewal.

Conclusion

Insured Declared Value plays a central role in determining both your insurance premium and claim settlement.

Understanding how insurance companies calculate IDV allows policyholders to select appropriate coverage and avoid financial loss during total loss situations.

Reviewing IDV at each renewal can help ensure that your policy remains aligned with your vehicle’s market value.

Author Bio

Ali Hassan is a financial content researcher specializing in insurance awareness for vehicle owners in Pakistan. His work focuses on simplifying policy terms and helping readers make informed decisions.

Sources / References

- Securities and Exchange Commission of Pakistan (SECP)

- State Bank of Pakistan Insurance Guidelines

- Jubilee General Insurance Motor Policy

- EFU General Insurance Motor Insurance Terms

- Adamjee Insurance Underwriting Guidelines