Introduction (A Real-Life Problem Many Families Face)

Medical treatment costs in Pakistan are increasing every year. A single hospitalization due to an accident, surgery, or serious illness can cost anywhere between PKR 80,000 to PKR 500,000 or even more depending on the hospital and treatment required.

Most families are not financially prepared for such unexpected expenses. In many cases, people are forced to:

- Borrow money from relatives

- Take personal loans

- Sell savings or assets

- Delay necessary medical treatment

This financial stress can be avoided with proper planning — and this is where health insurance becomes important.

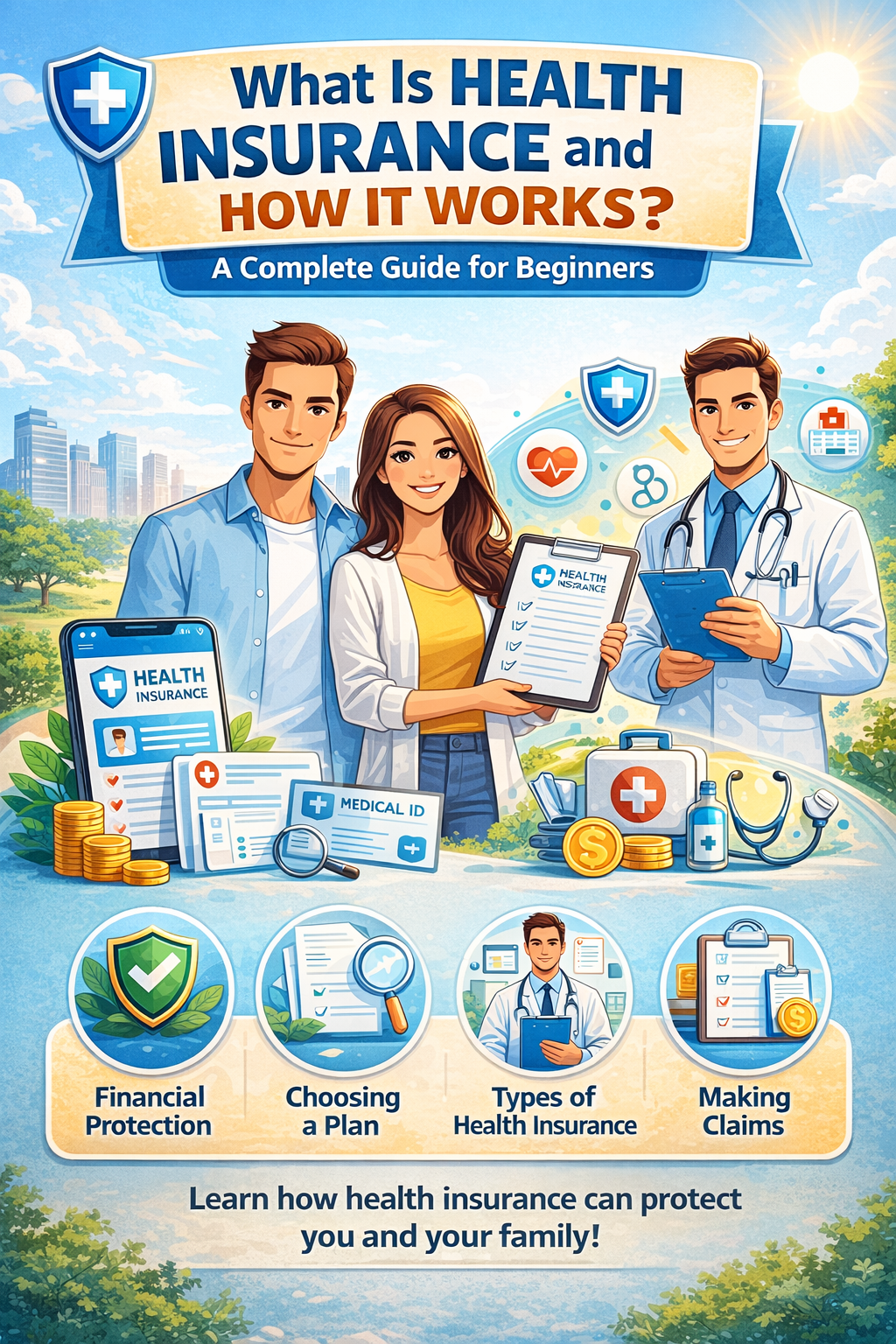

Health insurance helps you manage medical expenses by covering hospitalization, treatment costs, and other healthcare-related services depending on your selected plan. Instead of paying large medical bills from your own pocket, your insurance provider covers a significant portion of the expenses.

In this guide, you will learn what health insurance is, how it works, what it covers, who should buy it, how much it costs in Pakistan, and how you can choose the right plan based on your needs.

How Comprehensive Health Insurance Works

Health insurance is a financial agreement between you and an insurance company. You pay a fixed amount called a premium on a monthly or yearly basis. In return, the insurance company agrees to cover your medical expenses if you fall sick, get injured, or require hospitalization during the policy period.

Here’s how the process usually works:

Step 1: You purchase a health insurance policy

Step 2: You pay regular premium to keep the policy active

Step 3: If you require medical treatment, you inform your insurance provider

Step 4: The insurer covers eligible expenses as per policy terms

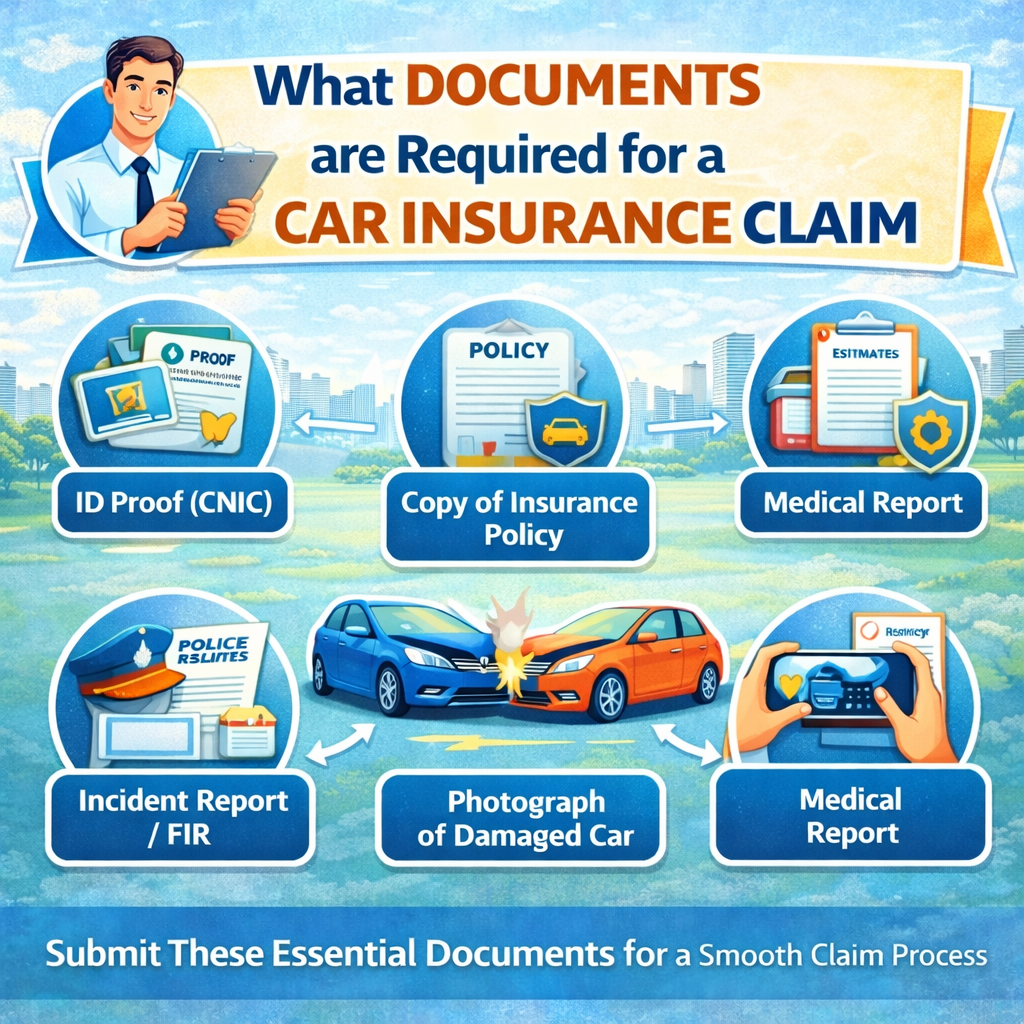

There are generally two claim methods:

Cashless Treatment

If you get treated at a network hospital associated with your insurance provider, the insurer directly settles the bill with the hospital. You do not need to pay the entire amount upfront.

Reimbursement Claim

If treatment is taken at a non-network hospital, you pay the expenses first and later submit documents to the insurer for reimbursement.

Who Should Buy Health Insurance?

Health insurance is useful for almost everyone, but it becomes especially important for:

- Individuals with families

- Self-employed professionals

- Freelancers

- Senior citizens

- People with limited savings

- Individuals with health risks

- Parents with dependent children

Even young and healthy individuals should consider buying insurance early because premiums are usually lower at a younger age and waiting periods for certain illnesses can be completed sooner.

Benefits of Health Insurance

Health insurance offers several important advantages:

Financial Protection

It protects your savings from being used for sudden medical emergencies.

Access to Quality Treatment

You can seek treatment at better hospitals without worrying about large expenses.

Cashless Hospitalization

Network hospitals allow direct billing between hospital and insurer.

Coverage for Major Illnesses

Policies may include coverage for surgeries, hospitalization, and diagnostic tests.

Peace of Mind

You can focus on recovery instead of financial stress during illness.

Tax Benefits

Certain health insurance premiums may qualify for tax deductions depending on regulations.

Limitations

Despite its benefits, health insurance also has certain limitations:

Waiting Period

Some illnesses may not be covered immediately after purchasing the policy.

Pre-Existing Conditions

Coverage for existing diseases may start after a specified waiting period.

Policy Exclusions

Certain treatments or conditions may not be included in standard plans.

Room Rent Limits

Some policies restrict hospital room charges.

Co-Payment Clause

You may need to share a percentage of treatment cost in some plans.

Understanding these limitations before buying a policy helps avoid claim rejections later.

Estimated Cost in Pakistan

Health insurance premiums in Pakistan vary depending on:

- Age of the insured person

- Coverage amount

- Medical history

- Policy type

- Insurance company

- Family size (for family plans)

Approximate yearly premium range:

- Individual Plan (Young Adult): PKR 12,000 to PKR 25,000

- Individual Plan (Middle Age): PKR 20,000 to PKR 40,000

- Family Plan: PKR 35,000 to PKR 80,000

Higher coverage limits or additional benefits may increase the premium.

Factors That Affect Premium

Insurance companies calculate premiums based on:

- Age

- Gender

- Medical history

- Lifestyle habits

- Coverage amount

- Policy duration

- Family size

- Add-on benefits

Older individuals or those with pre-existing medical conditions may be charged higher premiums due to increased health risks.

Real Example Scenario

Suppose a person without health insurance requires surgery costing PKR 200,000.

Without Insurance

The entire amount must be paid from personal savings.

With Insurance

If the person has a policy covering up to PKR 300,000, the insurance company may pay most of the treatment cost depending on policy terms.

This significantly reduces the financial burden during medical emergencies.

Tips Before Buying

Before purchasing a health insurance policy, consider the following:

- Choose adequate coverage amount

- Check hospital network list

- Understand waiting periods

- Review policy exclusions

- Compare premium options

- Confirm claim process

- Read policy wording carefully

Selecting the right policy ensures better financial protection and smoother claim settlement.

FAQs

What is health insurance?

Health insurance is a financial plan that covers medical expenses in case of illness or injury.

Is health insurance necessary for young people?

Yes, buying insurance early helps complete waiting periods and secure lower premiums.

Can I buy insurance for my entire family?

Yes, family health insurance plans are available.

Does health insurance cover all diseases?

Coverage depends on policy terms and waiting periods.

What happens if I miss premium payment?

Policy benefits may lapse if premium is not paid on time.

Conclusion

Health insurance is an essential financial safety tool that protects you from unexpected medical expenses. By paying a small premium regularly, you can avoid major financial stress during emergencies and access better healthcare services when needed.

Choosing the right policy based on your medical needs and financial capacity can help secure your health and savings in the long run.

Author Bio

Ali Raza is a financial and insurance content writer who focuses on simplifying health and motor insurance concepts for everyday readers in Pakistan.

Sources / References

- Securities and Exchange Commission of Pakistan (SECP) – Insurance Consumer Information

- State Bank of Pakistan – Financial Awareness Resources

- General Health Insurance Policy Documents from Insurance Providers in Pakistan